McDonald's. Rentabilidad, Paz, Tranquilidad.

Un 5-6% anual sobre el que duermo tranquilo.

Este artículo está disponible en español e inglés.

Índice.

Hoy quiero dejar un poco de lado la IA, el petróleo, los chips y el SaaSmageddon, para buscar un poco de paz y tranquilidad 🧘Eso es justo lo que siento cuando entro a un establecimiento de McDonald’s sabiendo que el 4% de mi cartera está en esta acción. Me siento en una mesa, y busco la oferta del día en la aplicación. Y por 3~4 euros, me como una hamburguesa pequeña y unas patatas.

Cuando voy de viaje a otro país, a menudo tengo problemas para comunicarme porque mi inglés es nefasto. Y probablemente me pierda y no sepa utilizar el transporte público porque tengo el instinto de supervivencia de un lemming.

Pero sé que allí me voy a encontrar un McDonald’s donde podré comer y descansar un rato. Un refugio. Un hogar. Y un pellizquito de ese refugio, es mío.

Por eso sigo acumulando la acción que más tranquilidad me da en mi cartera (con permiso de Berkshire). Y aunque tengo bastante ya MCD 0.00%↑ , estoy deseando que siga cayendo para seguir acumulando. Voy a explicar los números detrás de esa tranquilidad.

El Precio, en Contexto

MCD cotiza ahora mismo con un PER de entorno a 22-23x. Eso es entre un 10% y un 13% por debajo de su media de los últimos 3, 5 y 10 años, que ronda las 25-26x. No es un chollo histórico tipo covid-crash, pero sí es de los múltiplos más bajos que ha tenido la acción en bastante tiempo.

Un PER 22 en una empresa que crece ingresos al 3-4% anual no es barato en términos absolutos. Es barato en términos relativos a su propia historia.

Encontrando la Rentabilidad Esperada a Partir del Cost of Equity

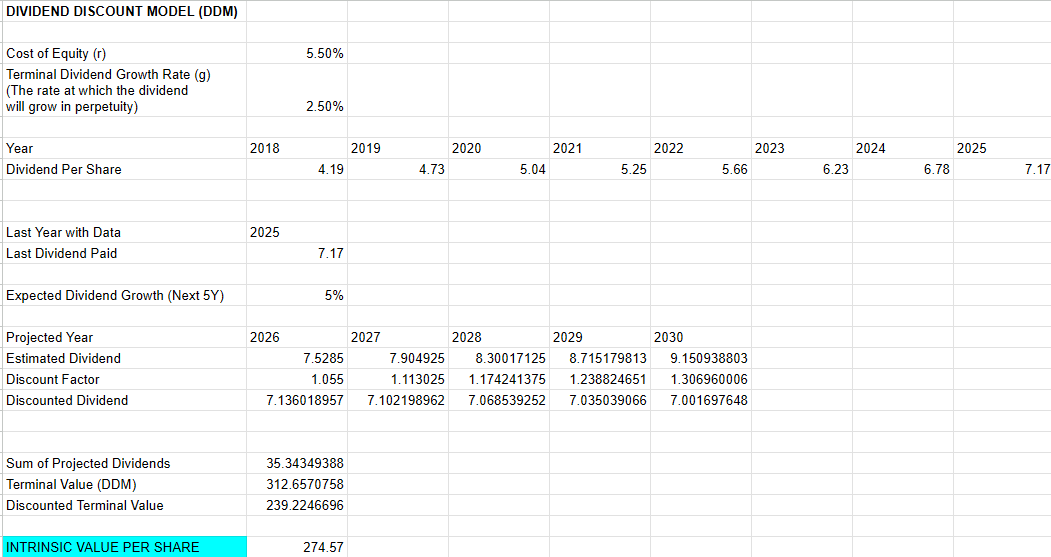

Puesto que McDonald’s es una dividendera clásica, voy a empezar realizando un Dividend Discount Model. En este caso la idea no es utilizar el cost of equity consensuado por los analistas, sino forzar un cost of equity que ajuste el valor intrínseco al valor actual de la acción. Puesto que en el DDM se descuentan flujos que van a parar al accionista (no a los acreedores), una vez despejada la X del cost of equity para valor intrínseco igual a valor actual, podemos tomar ese cost of equity como el retorno anual para el accionista comprando al precio actual de la acción. Esto es lo que se llama implied cost of capital — y como decíamos, a diferencia del DCF, en un DDM ese número sí equivale al retorno total que puedo esperar como accionista (dividend yield + crecimiento), si mis proyecciones de dividendo se cumplen.

He utilizado un crecimiento esperado del dividendo a 5 años del 5%. Bastante conservador, porque si miramos el crecimiento de los últimos años, vemos que ha sido superior.

Usamos Terminal Dividend Growth Rate (g) 2.5%.

Con esta configuración, para obtener un valor intrínseco parecido al precio actual, necesitamos un cost of equity de aproximadamente 5.5%. Puesto que hemos hecho algunas estimaciones como un g de 2.5% y un crecimiento de dividendo de 5% para los próximos 5 años, es preferible tratarlo como un rango (5-6%) más que como un número con decimales de precisión. Y ese rango sería nuestra estimación de la rentabilidad que podemos esperar de McDonald's.

¿Es Eso Mucho o Poco? El Dato Incómodo

El bono del Tesoro americano a 10 años cotiza ahora mismo en torno al 4.5-4.6%. Si aplico el modelo estándar para estimar cuánto retorno debería exigir el mercado a una acción como MCD (CAPM: risk-free + beta × prima de riesgo), con una beta razonable para MCD (0.6-0.7, la que reportan la mayoría de proveedores de datos), sale un cost of equity “teórico” de en torno al 7-7.5%.

Es decir: el mercado, al precio actual, solo me está pagando un 5-6% de retorno esperado vía dividendo y crecimiento, cuando el riesgo sistemático de la acción, según el modelo estándar, justificaría exigir más, cerca del 7-7.5%. El mercado paga muy poca prima por el riesgo de McDonald’s, porque valora tanto la previsibilidad y el perfil “bono-proxy” del negocio, que le perdona parte de esa prima que otro tipo de acciones sí tendría que ofrecer.

Entonces, ¿Por Qué Sigo Comprando?

Porque ese 5-6% no es un mal retorno para el nivel de riesgo real que percibo en el negocio, aunque el CAPM de manual diría que debería exigir más. Y sobre todo porque:

Es un negocio con foso competitivo brutal, poder de fijación de precios, un componente semi-inmobiliario (los alquileres a franquiciados son básicamente una renta), y una previsibilidad de caja que muy pocas empresas del mundo tienen.

Ese retorno no depende de que el mercado me re-rate el múltiplo. Depende solo de crecimiento orgánico + dividendo, que es justamente el tipo de retorno que menos me falla cuando las cosas se ponen feas en el resto de la cartera.

Porque se ha comportado bien en momentos complicados para el mercado, por ejemplo el 2008.

Y esto es lo más importante para mí: es la posición que me deja dormir. No la compro por asimetría de rentabilidad, la compro porque a este precio el retorno esperado, aunque modesto, viene con muchísima menos incertidumbre que en casi cualquier otro sitio donde podría poner ese dinero.

Discounted Cash Flow Para Comparar con la Competencia

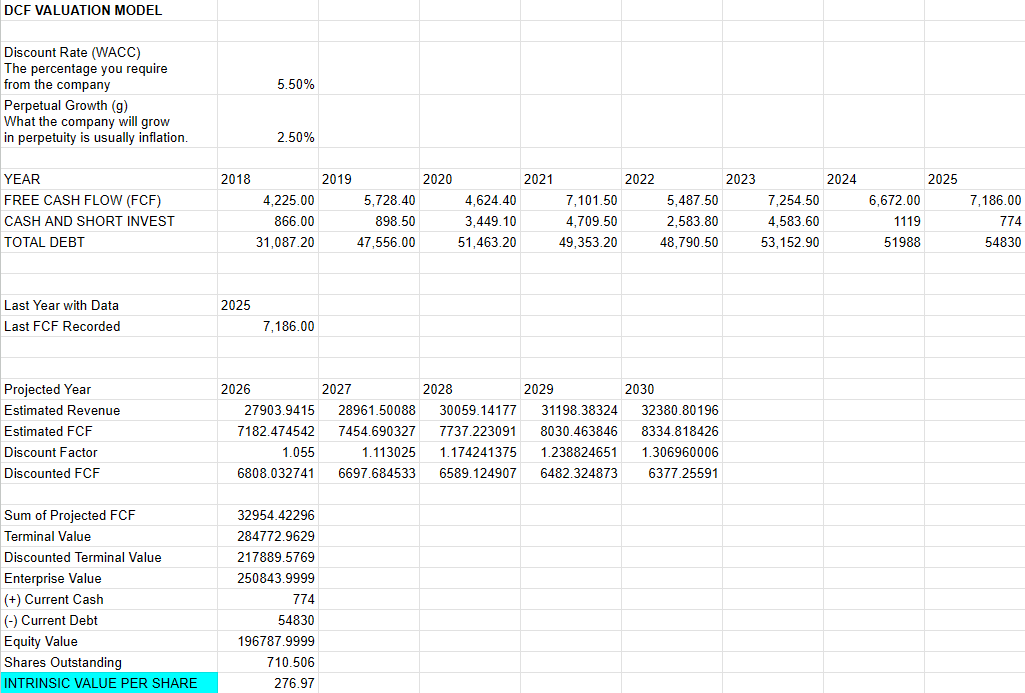

Voy a hacer un ejercicio parecido con un DCF clásico. Usaré un crecimiento de revenue del 3.79%, media desde 2018, y margen de conversión de revenue a FCF del 25.74%, también media desde 2018. Y un valor terminal g del 2.5%.

Y con estos valores voy a buscar un WACC con el que obtenga un valor intrínseco similar al precio actual:

Curiosamente obtengo un WACC similar al cost of equity del DDM. No podemos asumir que el WACC equivale a la rentabilidad anual para el accionista porque en el WACC va incluido lo que la empresa tiene para el accionista y para los acreedores (por ejemplo para los bonistas). Sin embargo es curioso que salga un valor similar al cost of equity del DDM. Entiendo que esto es debido a que, a pesar de que McDonald’s tiene bastante deuda, genera tanto flujo de caja, que pagar la deuda no es un problema (y que probablemente se financie bastante barato). Además hay que tener en cuenta que utilicé un crecimiento del dividendo muy conservador, de 5% solamente.

En cualquier caso mi objetivo era más obtener un WACC para el precio actual de la acción, por un lado para compararlo con el WACC consensuado por analistas para McDonald’s, que se sitúa entre 7~7.5%. Y por otro para compararlo con competidores como QSR o Starbucks.

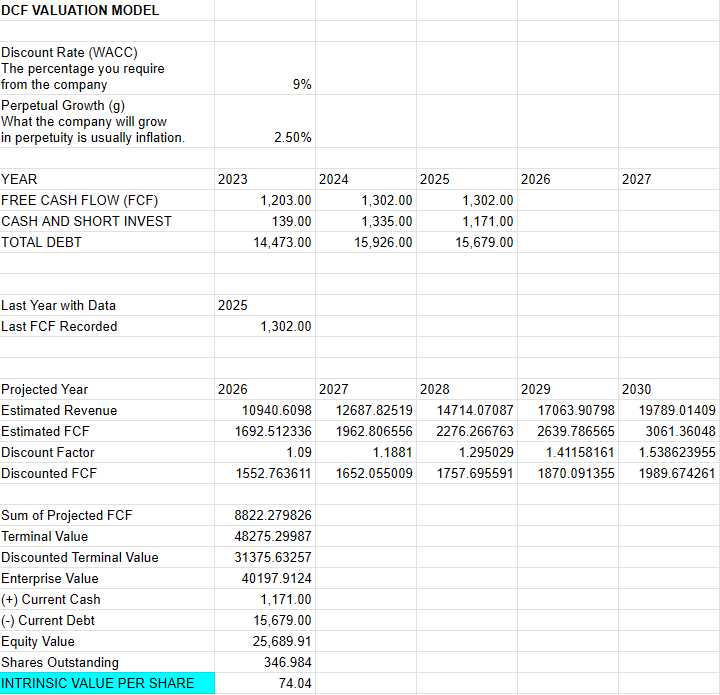

En el caso de QSR, si realizo el mismo ejercicio, obtengo un WACC del 9% para ajustar el valor intrínseco al precio actual:

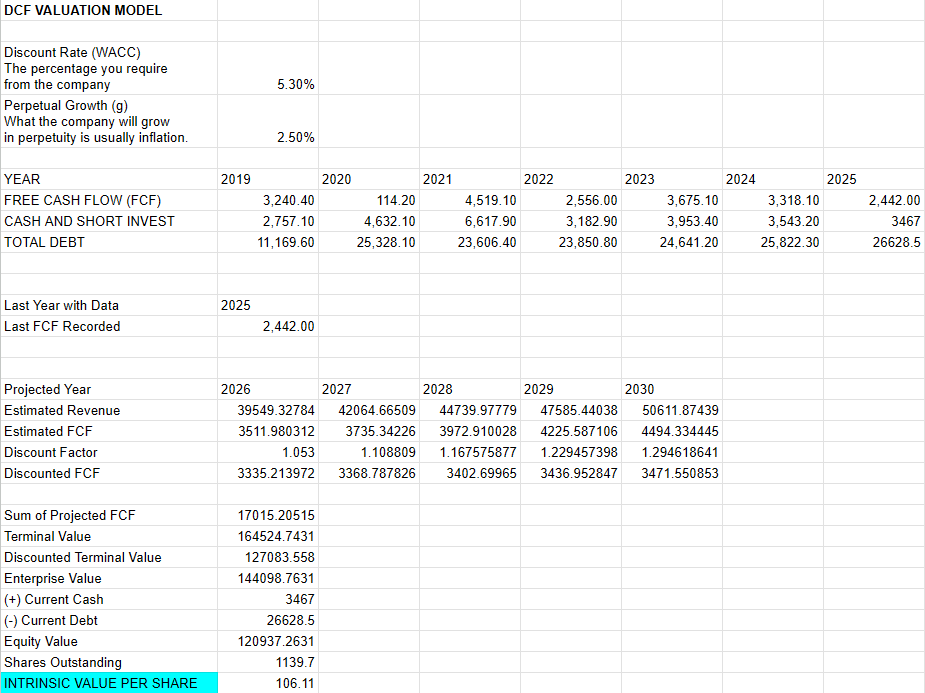

Para Starbucks obtengo un WACC del 5.3%:

Por lo tanto, si hacemos el ejercicio de buscar un WACC que fuerce el valor intrínseco al precio actual, obtenemos un WACC del 9% para QSR, del 5.5% para MCD y del 5.3% para SBUX, al precio en que se realizaron los cálculos.

Esto podría darnos una idea de que QSR podría estar más barata que MCD y SBUX. De hecho, haciendo el ejercicio que hicimos con el DDM para QSR, obtengo una rentabilidad anual del 6.3%, y para SBUX, del 5.2%.

¿Entonces, Por Qué MCD y no QSR?

McDonald’s no es solo una empresa de comida rápida, es un cartel inmobiliario. Compra o alquila los terrenos y locales más codiciados del mundo y los subalquila a sus franquiciados. Esto le asegura ingresos estables por alquiler y regalías que no dependen únicamente de la venta de hamburguesas.

QSR utiliza más un modelo puramente de franquicia, careciendo de este gigantesco portafolio de bienes raíces.

Por otro lado, gracias a su escala global y a su estructura de negocio, MCD tiene márgenes operativos líderes en el sector. MCD históricamente mantiene márgenes operativos cercanos al 46%, mientras que QSR suele rondar márgenes operativos próximos al 26%. MCD necesita generar menos crecimiento de ventas para obtener el mismo beneficio neto que sus competidores.

Además tiene una fortaleza de marca y escala superiores. McDonald’s es una de las marcas más reconocidas del mundo. Esto se traduce en un tráfico masivo y un poder de negociación con proveedores que cadenas como Burger King, Popeyes o Tim Hortons (marcas de QSR) no tienen.

Conclusión y Cuidadín

No todas las posiciones de una cartera tienen que ser la mejor idea de rentabilidad-riesgo del mundo. Algunas están para dar rentabilidad ajustada al riesgo bajo, previsibilidad, y sobre todo, paz mental para poder mantener el resto de la cartera con la cabeza fría cuando las cosas se ponen feas en otro sitio. MCD, para mí, es eso. Un ~5-6% anual, con esta calidad de negocio detrás, es un retorno por el que firmo. Y si el precio sigue cayendo, la ecuación solo mejora — sigo ampliando.

Sea como sea, como siempre, esto no es ninguna recomendación de compra. Ninguna empresa es 100% segura y mañana mismo la narrativa del mercado puede cambiar por completo con respecto a McDonald’s, como ya cambió con respecto a otros pesos pesados, como la infame Diageo. Si mañana una bacteria rarísima afecta a un montón de consumidores de McDonald’s, se va a liar. Si los chavales dejan de comer hamburguesas como supuestamente han dejado de beber o fumar (o al menos el mercado compra esa narrativa), se va a liar. Si Ozempic nos pone a todos a dieta, se va a liar. Así que como siempre, haced vuestro propio análisis y valorad los riesgos.

Un saludo a todos.

English Version

McDonald's. Returns, Peace, Tranquility.

A 5-6% annual return I can sleep soundly on.

Today I want to leave AI, oil, chips, and SaaSmageddon aside for a bit, to find a little peace and quiet 🧘 That’s exactly what I feel when I walk into a McDonald’s knowing that 4% of my portfolio is in this stock. I sit down at a table, check the app for today’s deal. And for 3~4 euros, I eat a small burger and some fries.

When I travel to another country, I often struggle to communicate because my English is terrible. And I’ll probably get lost and have no idea how to use public transport, because I have the survival instincts of a lemming.

But I know that there, I’ll find a McDonald’s where I can eat and rest for a while. A refuge. A home. And a little piece of that refuge is mine.

That’s why I keep accumulating the stock that gives me the most peace of mind in my portfolio (with all due respect to Berkshire). And even though I already own quite a bit, I’m hoping it keeps falling so I can keep buying more. Let me walk you through the numbers behind that peace of mind.

The price, In Context

MCD is currently trading at a PE ratio of around 22-23x. That’s somewhere between 10% and 13% below its 3, 5, and 10-year average, which sits around 25-26x. It’s not a historic bargain like a covid-crash moment, but it is one of the lowest multiples the stock has traded at in quite a while.

A PE of 22 for a company growing revenue at 3-4% a year isn’t cheap in absolute terms. It’s cheap relative to its own history.

Finding The Expected Return Through Cost of Equity

Since McDonald’s is a classic dividend payer, I’ll start by running a Dividend Discount Model. In this case, the idea isn’t to use the cost of equity consensus among analysts, but to force a cost of equity that makes the intrinsic value match the current share price. Since a DDM discounts cash flows that go directly to the shareholder (not to creditors), once you solve for X — the cost of equity that makes intrinsic value equal to current price — you can treat that cost of equity as the annual return for a shareholder buying at today’s price. This is what’s called implied cost of capital — and as we said, unlike a DCF, in a DDM that number really does equal the total return I can expect as a shareholder (dividend yield + growth), assuming my dividend projections hold.

I used an expected dividend growth rate of 5% over the next 5 years. Pretty conservative, since if you look at recent growth, it’s actually been higher.

We use a Terminal Dividend Growth Rate (g) of 2.5%.

With this setup, to get an intrinsic value close to the current price, we need a cost of equity of approximately 5.5%. Since we made some estimates here — a g of 2.5% and dividend growth of 5% for the next 5 years — it’s better to treat this as a range (5-6%) rather than a number with decimal-point precision. And that range would be our estimate of the return we can expect from McDonald’s.

Is That a Lot or a Little? The Uncomfortable Part

The 10-year US Treasury is currently trading around 4.5-4.6%. If I apply the standard model to estimate what return the market should demand from a stock like MCD (CAPM: risk-free rate + beta × risk premium), using a reasonable beta for MCD (0.6-0.7, what most data providers report), I get a “theoretical” cost of equity of around 7-7.5%.

In other words: at the current price, the market is only paying me a 5-6% expected return via dividend and growth, when the stock’s systematic risk, according to the standard model, would justify demanding more — closer to 7-7.5%. The market is paying very little risk premium for MCD, likely because it values the predictability and “bond-proxy” profile of the business so highly that it forgives part of the premium that other types of stocks would have to offer.

So Why do I Keep Buying?

Because that 5-6% isn’t a bad return for the actual level of risk I perceive in the business, even if textbook CAPM says I should demand more. And above all, because:

It’s a business with a brutal competitive moat, pricing power, a semi-real-estate component (the rent it charges franchisees is basically a landlord’s income), and a predictability of cash flow that very few companies in the world have.

That return doesn’t depend on the market re-rating the multiple. It depends only on organic growth + dividend, which is exactly the kind of return that fails me least when things get ugly elsewhere in the portfolio.

Because it’s held up well during rough patches for the market — 2008, for example.

And this is the most important part for me: it’s the position that lets me sleep at night. I don’t buy it for asymmetric upside, I buy it because at this price, the expected return, modest as it is, comes with far less uncertainty than almost anywhere else I could put that money.

A Discounted Cash Flow to Compare Against the Competition

I’ll run a similar exercise with a classic DCF. I’ll use a revenue growth rate of 3.79% (average since 2018) and a revenue-to-FCF conversion margin of 25.74% (also average since 2018). And a terminal g of 2.5%.

With these inputs, I’ll solve for the WACC that produces an intrinsic value close to the current price:

Interestingly, I get a WACC similar to the DDM’s cost of equity. We can’t assume that WACC equals the annual return for the shareholder, because WACC bundles together what belongs to the shareholder and what belongs to the creditors (bondholders, for example). Still, it’s curious that a similar number comes out of both. I think this is because, even though McDonald’s carries plenty of debt, it generates so much cash flow that servicing that debt isn’t a problem (and it’s probably financed pretty cheaply). It’s also worth noting I used a very conservative dividend growth assumption — just 5%.

Either way, my goal here was mostly to get a WACC for the current share price so I could compare it, on one hand, with the analyst-consensus WACC for McDonald’s, which sits between 7~7.5%. And on the other hand, to compare it against competitors like QSR and Starbucks.

For QSR, running the same exercise, I get a WACC of 9% to make intrinsic value match the current price:

For Starbucks, I get a WACC of 5.3%:

So, running the exercise of solving for the WACC that forces intrinsic value to match the current price, we get a WACC of 9% for QSR, 5.5% for MCD, and 5.3% for SBUX, at the prices these calculations were done.

This might suggest that QSR could be cheaper than both MCD and SBUX. In fact, running the same DDM exercise for QSR gives me an annual return of 6.3%, and for SBUX, 5.2%.

So Then, why MCD and not QSR?

McDonald’s isn’t just a fast-food company, it’s a real estate cartel. It buys or leases the most coveted land and locations in the world and subleases them to its franchisees. This guarantees stable rental income and royalties that don’t depend solely on burger sales.

QSR relies more on a pure franchise model, lacking this massive real estate portfolio.

On top of that, thanks to its global scale and business structure, MCD has industry-leading operating margins. MCD historically runs operating margins close to 46%, while QSR tends to hover around 26%. MCD needs less sales growth to generate the same net profit as its competitors.

It also has superior brand strength and scale. McDonald’s is one of the most recognized brands in the world. That translates into massive foot traffic and supplier bargaining power that chains like Burger King, Popeyes, or Tim Hortons (QSR’s brands) simply don’t have.

Conclusion, and a Word of Caution

Not every position in a portfolio has to be the best risk-reward idea in the world. Some exist to provide low-risk, risk-adjusted return, predictability, and above all, peace of mind — so you can keep a cool head on the rest of the portfolio when things get ugly elsewhere. For me, MCD is that. A ~5-6% annual return, backed by this quality of business, is a return I’ll happily sign up for. And if the price keeps falling, the equation only gets better — I keep adding.

Either way, as always, this is not investment advice. No company is 100% safe, and tomorrow the market narrative around McDonald’s could flip completely, just as it did with other heavyweights, like the infamous Diageo. If some rare bacteria hits a bunch of McDonald’s customers tomorrow, it’s going to get messy. If kids stop eating burgers the way they supposedly stopped drinking or smoking (or at least the way the market has bought into that story), it’s going to get messy. If Ozempic puts everyone on a diet, it’s going to get messy. So, as always, do your own research and weigh the risks.

Cheers to all.