What if Berkshire Had Bought Google With Applecoins Instead of Dollars? Would It Still Look Expensive?

Changing the denominator changes the whole story.

There’s been plenty of noise around Greg Abel’s decision to build a $26+ billion position in Alphabet. The most repeated criticism: Google is expensive. Measured in dollars, maybe.

But there’s another way to look at it.

Berkshire has spent years trimming Apple. If we assume that capital is looking to maintain quality growth exposure — not exit the asset class, but rotate within it — then the relevant question changes entirely.

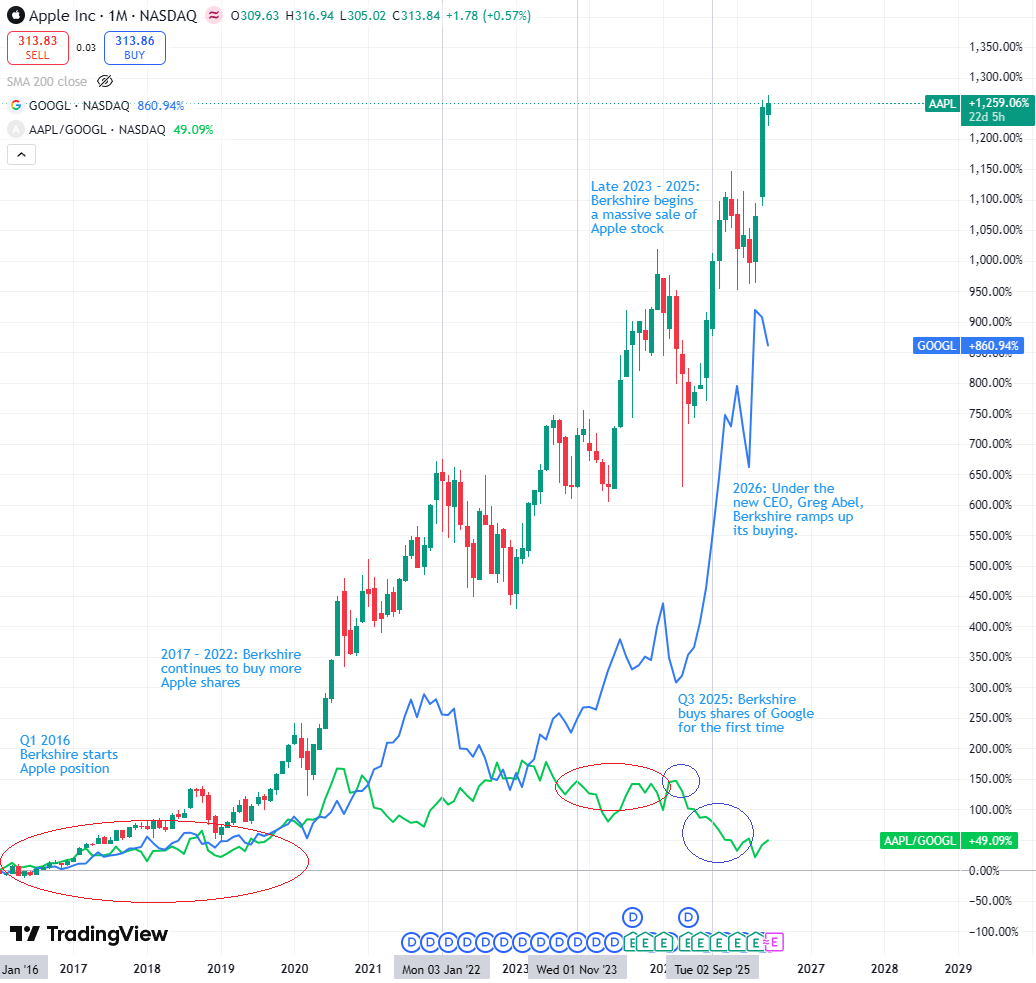

Imagine you lived in a country where you don’t pay in dollars, euros, or yuan. You pay in fractions of Apple. Call it The Republic of Berkshire. Then the question isn’t how many dollars you pay for Google, but how many Apple units you pay for one Google unit. Something like the $AAPL/$GOOGL ratio.

Right now, that ratio sits at roughly 1.19x — one share of Google costs about 1.2 shares of Apple. Not exactly a stretched premium for a business trading at a lower P/E (28x) than the Apple it’s replacing (37x), with a cloud backlog above $460 billion and AI infrastructure spend set to nearly double in 2026.

Seen that way, this isn’t buying expensive growth against cash. It’s a rotation within the growth sleeve — from a mature compounder with massive buybacks to one with a different engine: AI infrastructure, cloud, search — at a relative price that looks entirely reasonable.

Apple (AAPL) Timeline

Q1 2016: Berkshire Hathaway reveals its very first purchase of Apple shares.

2017 – 2022: Berkshire continues to buy more shares. Apple becomes the largest holding in its portfolio.

Late 2023 – 2025: Warren Buffett begins a massive sale of Apple stock. Berkshire cuts its stake by about 74% to take over $100 billion in profits.

Google (Alphabet / GOOGL) Timeline

Q3 2025: Berkshire Hathaway buys shares of Google for the first time. It starts with about 17.8 million shares.

2026: Under the new CEO, Greg Abel, Berkshire ramps up its buying.

There’s also a structural factor that gets overlooked too easily: Berkshire can’t buy just anything. At the scale it operates, the universe of viable targets is small. Alphabet is one of the few assets that can absorb $26 billion without the market moving against you on the way in.

Criticizing the purchase by looking at the P/E in dollar terms is only half the analysis. The other half lives in The Republic of Berkshire — where they pay in Applecoins.