Haciendo las Paces con los Bonos: El Amortiguador Antisustos de tu Cartera

Comprender los bonos puede dar estabilidad a tu cartera y ahorrarte un par de sustos. Vamos allá!

Este artículo está disponible en español e inglés.

English version below ↓

Muchos inversores ignoran por completo los bonos y ni siquiera se molestan en entender su funcionamiento. Pero los bonos son posiblemente el activo más importante del mercado, el que más lo mueve y, en buena medida, el que condiciona toda la economía.

Predecir el comportamiento de este activo es posiblemente una de las tareas más difíciles para un inversor, junto con el comportamiento de las divisas (de hecho, invertir en bonos implica, de forma indirecta, invertir en divisas: de nada sirve comprar bonos de un país al 4% de interés si la divisa de ese país cae un 8%). Predecir el comportamiento de los bonos implica predecir factores macroeconómicos, políticos del país del bono, así como factores geopolíticos e internacionales. En mi humilde opinión, casi nadie puede ver con certeza hacia dónde irán los tipos de interés de un país.

Sin embargo, una cartera diversificada debe tener bonos que te protejan en ciertos escenarios y ciclos económicos, por ejemplo en una etapa prolongada de recesión o para amortiguar un crash por un cisne negro.

En mi cartera, considerando la situación actual donde la renta variable podría estar bastante sobrecalentada, tengo una posición considerable en activos fuera de la renta variable (oro, bonos, materias primas, liquidez...). En concreto, mi posición actual en bonos asciende a un sustancial 30% de la cartera.

Puesto que considero tremendamente difícil adivinar hacia dónde irán los tipos de interés y las divisas de cada país, toda mi posición en bonos la tengo a través de un ETF que sigue el Bloomberg Aggregate Bond Index. El Bloomberg Aggregate Bond Index está compuesto principalmente por bonos gubernamentales, corporativos y respaldados por hipotecas de alta calidad crediticia, los cuales se diversifican de forma equilibrada a través de diferentes sectores económicos, regiones geográficas y plazos de vencimiento (duración). Esta variedad de plazos y emisores permite capturar el comportamiento general de la renta fija segura, reduciendo el riesgo y ofreciendo una imagen clara de cómo se mueve el mercado de deuda a nivel global o regional.

iShares Core Global Aggregate Bond UCITS ETF

El ETF que utilizo para invertir en bonos es el ETF AGAC de BlackRock: iShares Core Global Aggregate Bond UCITS ETF:

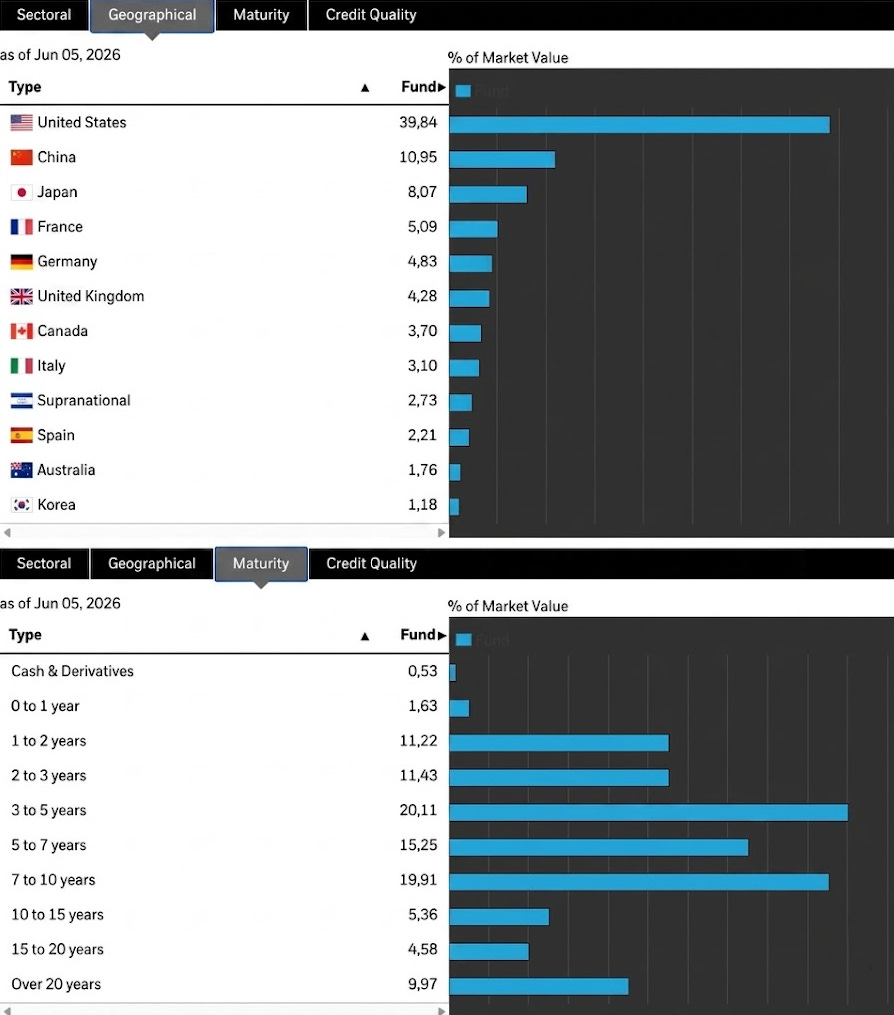

El ETF está diversificado en bonos gubernamentales y corporativos de distintos países y duraciones, predominando los bonos estadounidenses, y teniendo una duración media de 6–7 años.

Y el “Lambo” para cuándo

Efectivamente, los bonos no te van a hacer trillonario. Los bonos son un tipo de activo que nos ofrece estabilidad, seguridad y menor volatilidad en la cartera, obviamente con una rentabilidad mucho más ajustada.

El problema es que muchas veces, cuando compramos un ETF de este tipo, es muy difícil calcular qué rentabilidad podemos esperar a medio plazo, al menos para un inversor retail como muchos de nosotros. No porque sea difícil estimar la rentabilidad de un bono. Todo lo contrario: cuando compras un bono, sabes de antemano, siempre y cuando no se produzca un impago, la rentabilidad que puedes obtener (a diferencia de la bolsa, donde necesitas hacer una estimación). Es difícil porque la cantidad de activos (bonos) que componen el ETF es altísima.

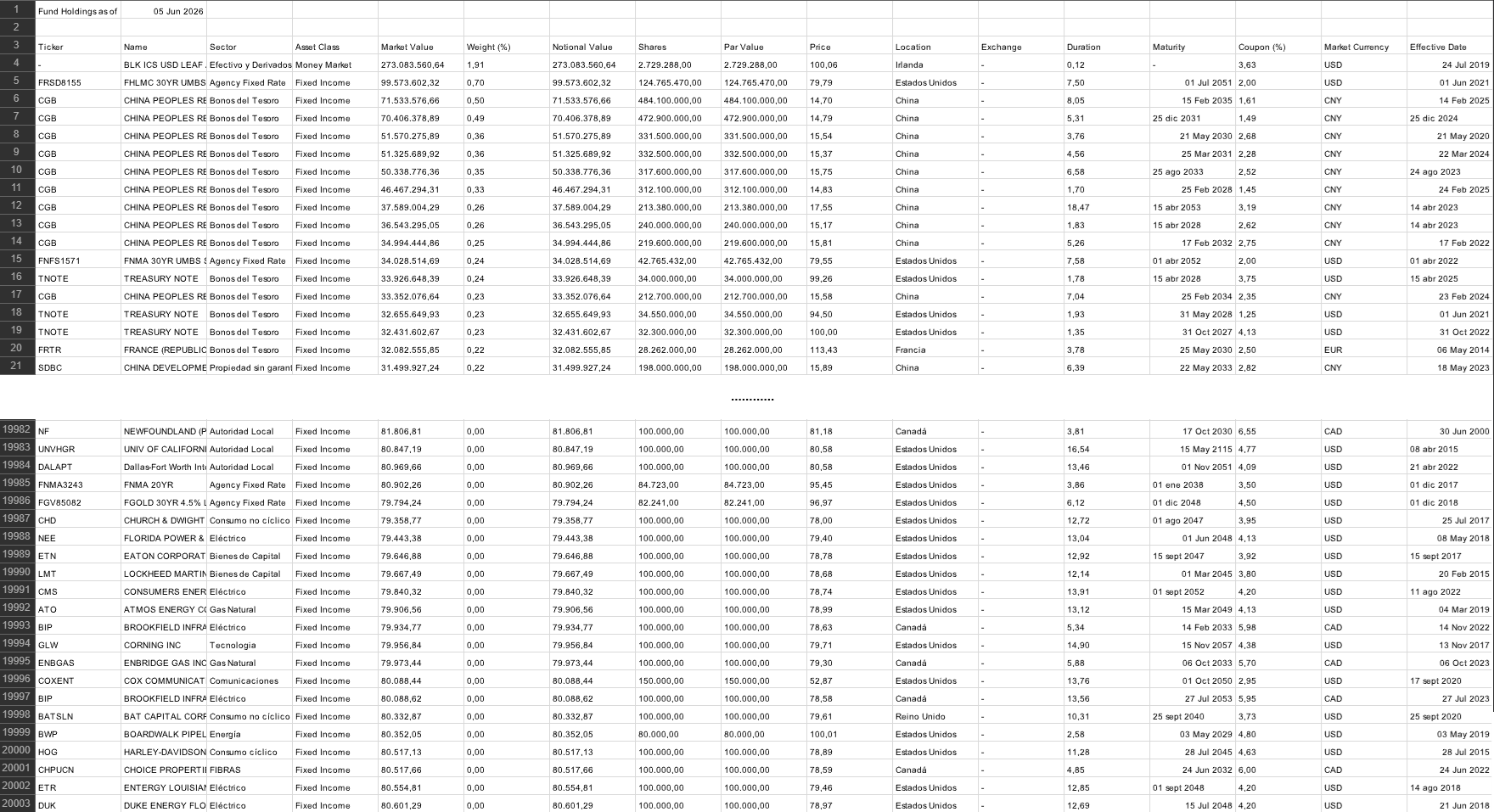

En la propia web de BlackRock podemos descargar un documento CSV con todos los holdings que componen el ETF AGAC y podemos observar que son en torno a 20.000 bonos diferentes.

Si quisiéramos calcular qué rentabilidad exacta nos ofrecen los bonos que componen el ETF necesitaríamos obtener la rentabilidad exacta de cada uno de ellos hoy mismo (al precio de mercado actual de ese bono, no nos basta con saber su cupón), para luego calcular una media de todas las rentabilidades (una media ponderada según el peso de cada bono en el total del ETF).

Quizás grandes empresas como BlackRock pueden realizar este cálculo en tiempo real sin problemas, pero para inversores retail como la mayoría de nosotros, esto es una tarea titánica.

Cálculo de la rentabilidad aproximada

Puesto que calcular la rentabilidad exacta, como comentábamos en el apartado anterior, se escapa a nuestras capacidades, necesitamos idear un plan para hacer un cálculo aproximado.

Como vimos en las capturas un poco más arriba, BlackRock nos ofrece en su web el porcentaje de bonos de cada país, así como el porcentaje de bonos por duración.

Aquí obviamente hay bonos gubernamentales y corporativos, y las rentabilidades de cada uno son diferentes.

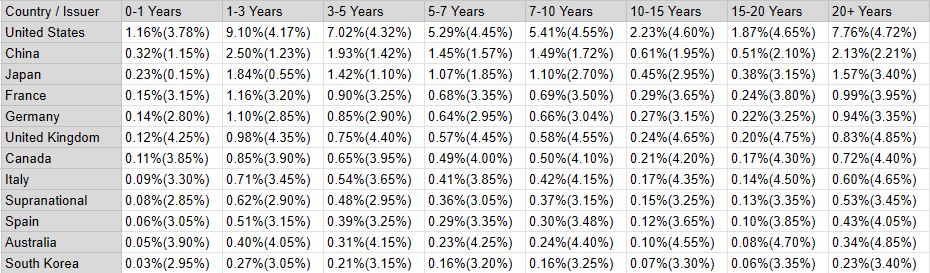

En nuestra aproximación lo que haremos será asumir que son bonos gubernamentales. Y lo que haremos será cruzar la tabla de peso por país con la tabla de peso por duración, para construir una matriz de pesos de cada par país-duración. Una vez construida dicha tabla, necesitaremos obtener la rentabilidad actual de los bonos para cada país y cada duración. Podríamos obtenerla, por ejemplo, en TradingView (si queremos ver la rentabilidad de los bonos de 30 años estadounidenses, buscaríamos el ticker US30Y. Para el de China a 20 años, CN20Y. Y así sucesivamente).

Puesto que tenemos 96 pares país-duración (habiendo tenido en cuenta solo los países que más pesan en el ETF), es un trabajo obtener manualmente cada rentabilidad (que además cambia con el precio del bono en el mercado). Así que hemos pedido a Gemini, la inteligencia de Google, que nos complete la tabla con las rentabilidades de cada país-duración.

En la captura anterior podemos observar que cada celda de la tabla corresponde al peso en el ETF de ese par país-duración y, entre paréntesis, la rentabilidad actual de esos bonos. Por ejemplo, el 1,16% del ETF corresponde a bonos estadounidenses de 0 a 1 años de duración, cuya rentabilidad ronda el 3,78%.

Con esta tabla, solo necesitamos calcular la media ponderada (en base a los pesos de cada par bono-duración en el ETF) de todas las rentabilidades.

Hemos pedido a Gemini que realice este cálculo y, según este, la rentabilidad media que nos ofrecen toda esta lista de bonos es aproximadamente del 3,61%.

Debemos tener en cuenta que hemos asumido que todos los bonos son gubernamentales y que, para cada par país-duración, hemos usado la rentabilidad del bono de ese país para esa duración. Los bonos corporativos ofrecen un extra de rentabilidad (porque también tienen un extra de riesgo frente a los gubernamentales). Así que posiblemente la rentabilidad real del ETF gire en torno al 4%.

Yield to Worst

A pesar de que hemos realizado este ejercicio para calcular una rentabilidad aproximada de nuestro ETF y para entender mejor en qué estamos invirtiendo, normalmente las empresas que emiten dicho ETF ya nos ofrecen algunas métricas que nos ahorran tener que hacer cálculos manualmente.

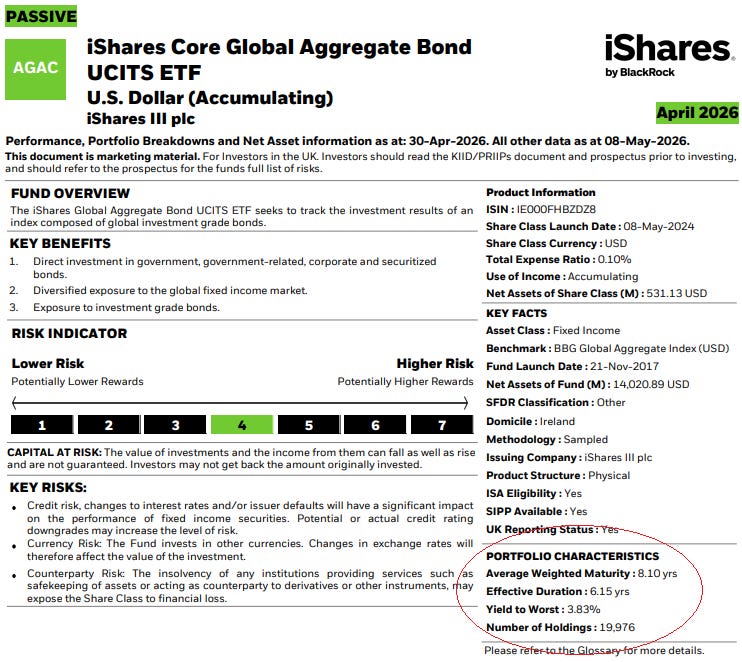

Si vamos al fact sheet del ETF AGAC, actualizado a abril de 2026, podemos ver algunas métricas que coinciden con nuestros cálculos:

Average Weighted Maturity: 8.10 yrs

Effective Duration: 6.15 yrs

Yield to Worst: 3.83%

Number of Holdings: 19976

El Yield to Worst (YTW) (que se podría traducir como “rentabilidad en el peor de los escenarios”) es una métrica clave en el mundo de la renta fija. Básicamente indica la mínima rentabilidad anualizada estimada que puedes esperar recibir de un bono o de una cartera de bonos (como este ETF), asumiendo que el emisor no quiebre.

Conclusión

Los bonos son un activo relativamente aburrido, y deben serlo, pero espero que este artículo no os haya resultado un ladrillo y que os haya ayudado a echar un poco de luz a un activo que muchos inversores desconocen o ignoran, pero que, en mi opinión, es importante no perder de vista y tener en nuestras carteras.

En cualquier caso, como siempre, esto no es un consejo de inversión, y cada uno debe estudiar y diseñar su propia cartera y decidir qué activos son apropiados para su perfil.

Si os ha gustado este artículo, suscribiros para recibir futuros posts en vuestro email. Saludos!

English Version.

Making Peace with Bonds: Your Portfolio’s Unsung Shock Absorber

Understanding bonds can stabilize your portfolio and save you from a few unpleasant surprises. Let’s go!

Many investors ignore bonds entirely and don’t even bother understanding how they work. Yet bonds are arguably the most important asset in the market — the one that moves markets and the broader economy more than anything else.

Predicting bond behavior is arguably one of the hardest tasks for any investor, right alongside predicting currency movements (and investing in bonds is implicitly investing in currencies: buying bonds from a country yielding 4% means nothing if that country’s currency drops 8%). Predicting bonds requires forecasting macroeconomic factors, country-specific political dynamics, and geopolitical conditions. In my humble opinion, almost no one can say with certainty where a country’s interest rates are headed.

That said, a well-diversified portfolio should include bonds that protect you in specific scenarios and economic cycles — think an extended recession, or a cushion against a black-swan crash.

In my own portfolio, given the current environment where equities may be quite overheated, I hold a substantial position in non-equity assets (gold, bonds, commodities, cash…). My current bond position stands at a meaningful 30% of the portfolio.

Since I consider it extremely difficult to predict where interest rates and currencies are heading, my entire bond exposure is through a single ETF that tracks the Bloomberg Aggregate Bond Index. This index is composed primarily of high-quality government, corporate, and mortgage-backed bonds, diversified across economic sectors, geographies, and maturities. That range of durations and issuers captures the overall behavior of safe fixed income, reduces risk, and provides a clear picture of how global (or regional) debt markets move.

iShares Core Global Aggregate Bond UCITS ETF

The ETF I use for bond exposure is BlackRock’s AGAC ETF: the iShares Core Global Aggregate Bond UCITS ETF:

The ETF is diversified across government and corporate bonds from multiple countries and maturities, with a heavy tilt toward U.S. bonds and an average duration of around 6–7 years.

So, when Lambo?

Indeed, bonds aren’t going to make you rich overnight. Bonds offer stability, security, and lower volatility in a portfolio — naturally, at the cost of lower returns.

The challenge is that when you buy this type of ETF, estimating your expected medium-term return is genuinely tricky, at least for retail investors like most of us. Not because estimating bond returns is inherently difficult — quite the opposite. When you buy a bond, you know upfront (assuming no default) exactly what return you’ll get. That’s very different from equities, where you’re always estimating. The difficulty here is that the ETF holds an enormous number of bonds.

On BlackRock’s own website you can download a CSV file with all the ETF’s holdings — and you’ll find roughly 20,000 different bonds.

To calculate the exact yield of all the bonds in the ETF, you’d need the current yield of each one (at today’s market price, not just the coupon), then compute a weighted average based on each bond’s weight in the portfolio. Large institutions like BlackRock can do this in real time. For retail investors, it’s a Herculean task.

Estimating the Approximate Yield

Since calculating the exact yield is beyond reach for most of us, we need a practical approximation.

As shown in the screenshots above, BlackRock provides both the country weight breakdown and the duration weight breakdown on their website.

The portfolio includes both government and corporate bonds, each with different yields.

For our approximation, we’ll assume all bonds are government bonds. The method: cross the country weight table with the duration weight table to build a country × duration weight matrix. Once that’s done, we need the current yield for each country-duration pair — which you can look up on TradingView (e.g., US30Y for the 30-year U.S. Treasury, CN20Y for China’s 20-year bond, and so on).

Since there are 96 country-duration pairs (considering only the ETF’s most significant country weights), manually retrieving each yield is tedious — especially since yields shift with bond prices daily. So I asked Gemini, Google’s AI, to populate the table with the relevant yields for each country-duration pair.

In the table above, each cell shows the ETF weight for that country-duration pair, with the current yield in parentheses. For example, 1.16% of the ETF consists of U.S. bonds with a 0–1 year duration, currently yielding around 3.78%.

With this table, the only remaining step is a weighted average of all yields (weighted by each bond’s share in the ETF).

I asked Gemini to run this calculation. The result: the weighted average yield across all these bonds is approximately 3.61%.

Keep in mind: we assumed all bonds are government bonds and used the sovereign yield for each country-duration pair. Corporate bonds carry an additional yield premium (reflecting their extra risk). So the ETF’s actual real-world yield likely hovers around 4%.

Yield to Worst

Even though we did this exercise to estimate an approximate yield and better understand what we’re actually invested in, ETF providers typically publish metrics that save us from having to do the math manually.

If you check the fact sheet for the AGAC ETF, updated to April 2026, you’ll find metrics that align closely with our estimates:

Average Weighted Maturity: 8.10 yrs

Effective Duration: 6.15 yrs

Yield to Worst: 3.83%

Number of Holdings: 19,976

Yield to Worst (YTW) — roughly “return in the worst-case scenario” — is a key fixed income metric. It represents the minimum annualized return you can expect from a bond or bond portfolio (like this ETF), assuming no default by the issuer.

Conclusion

I hope this post has helped shed some light on an asset class that many investors overlook — yet one that, in my view, deserves a place in any thoughtful portfolio.

As always, this is not investment advice. Everyone should study and design their own portfolio based on their individual risk profile.

Thanks for reading, and if you enjoyed this post, subscribe below!