De Pesca en el Ecosistema de los Pagos

Todo lo que necesitas saber sobre el ecosistema de pagos antes de pescar en él.

Este artículo está disponible en español e inglés.

English version below ↓

Se dice que a río revuelto, ganancia de pescadores. Y si te has dado una vuelta por redes sociales o por las noticias sobre economía e inversión, ya te habrás dado cuenta de que todo el ecosistema de los pagos está bastante revuelto:

Competencia feroz entre actores tradicionales y nuevos entrantes.

Disrupción tecnológica constante.

Criptomonedas y stablecoins empujando desde fuera del sistema.

Bancos centrales liándola parda con sus propias iniciativas digitales.

Regulación y control fiscal apretando cada vez más.

Pagos A2A (account to account), ofrecidos por algunos adquirentes para pagar directamente con el banco, de una cuenta a otra, saltándose gran parte del ecosistema tradicional, dejando fuera, por ejemplo, a Visa y Mastercard.

Pagos Closed-Loop de saldo a saldo dentro de la misma aplicación.

Inteligencia artificial rediseñando procesos que llevaban décadas sin tocarse.

Y hasta el “tap to pay“, que convierte el móvil en un datáfono y deja fuera aparatos que antes eran imprescindibles.

Es un mundo que yo diría que es sencillo en el fondo, porque todo tiene su lógica cuando lo entiendes. Pero en el que ahora mismo está todo un poco liado. Algo que en principio parece simple (”doy la orden para que el dinero de la fuente X, normalmente una cuenta bancaria, aparezca en el destino Y, también una cuenta bancaria habitualmente”) se ha convertido, con décadas de desarrollo por parte de distintos actores, en un Frankenstein con muchas capas de funcionalidad encima.

Cuando ves todo el ecosistema junto, la sensación que da es que podría simplificarse enormemente. Y ese es, en mi opinión, el mayor peligro estructural para muchas de las empresas del sector. Con las redes y las tecnologías que había hace dos décadas, todo tenía sentido. Pero con la tecnología que existe hoy, servidores tremendamente potentes y un mundo 100% interconectado con redes veloces, mucha de la funcionalidad parece redundante — capas que podrían eliminarse o colapsarse, dejando fuera a actores que hoy cobran por estar en medio.

En próximos posts voy a analizar varias empresas de este sector, y este artículo es una introducción necesaria para entender el ecosistema de los pagos de forma general. En las próximas secciones intentaré dar una visión global del mismo.

⚠️ Aviso a navegantes: se viene ladrillazo ⚠️

Las próximas secciones podrían ser un poco espesas, pero creedme que merece la pena tener un poco de paciencia, porque una vez tienes el contexto y entiendes todo el ecosistema de pagos, es mucho más fácil entender el porqué de cada empresa, qué hace cada una, cómo de importante es y por qué tiene moat o no, o por qué peligra su existencia.

Movimientos B2B: Banco-Banco

La base de todo este ecosistema es la transferencia de capital entre bancos, desde una cuenta bancaria hasta otra. El resto de capas (toda la red para pagos con tarjeta de Visa o Mastercard, los adquirentes como Adyen o Fiserv, los pagos A2A, etc…) al final podrían considerarse complementos para facilitar y hacer más cómodas y seguras estas transferencias entre cuentas bancarias.

“Transferencia entre cuentas bancarias” suena a algo sencillo, y en realidad debajo hay una infraestructura brutal que poca gente conoce.

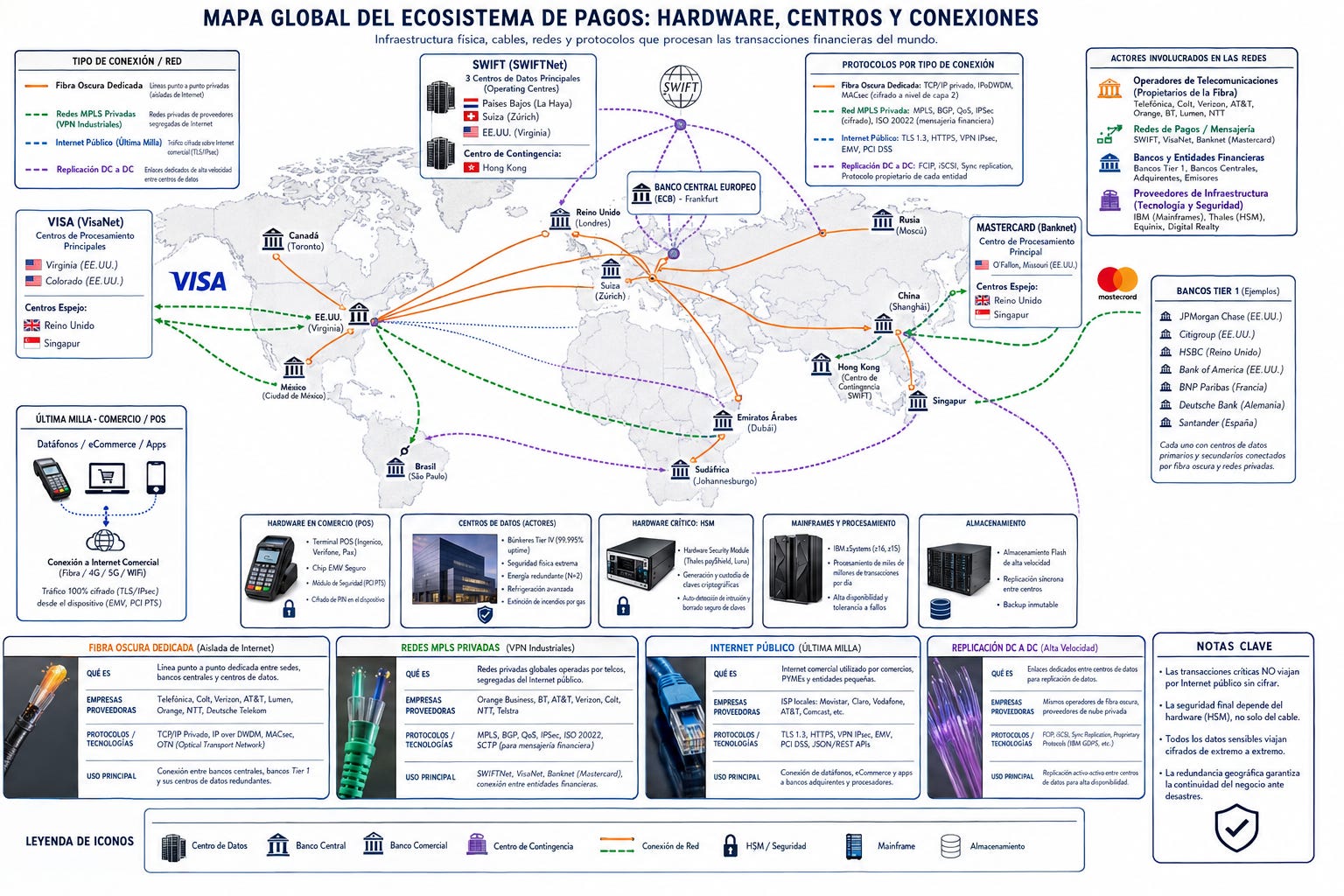

Lo primero que hay que entender es que los bancos no se comunican por el mismo internet que usas para ver Netflix. Los grandes bancos (los llamados Tier 1: JPMorgan, Citigroup, BNP Paribas, Bank Of America, Santander...) y los bancos centrales usan lo que se conoce como fibra oscura: filamentos de fibra óptica alquilados a largo plazo a operadoras de telecomunicaciones que están dedicados exclusivamente a ese tráfico. Nadie más pasa por ahí. Es literalmente un tubo de luz privado del punto A al punto B. De esta manera consiguen aislar la red y evitar en gran medida problemas de ciberseguridad.

Para conexiones internacionales entre las instituciones financieras más importantes, la historia es parecida pero a mayor escala. SWIFT (la cooperativa que conecta a más de 11000 instituciones financieras de todo el mundo) no se ha dedicado a tirar sus propios cables cruzando el Atlántico. Sin embargo sí opera su propia red privada global (SWIFTNet, una VPN de escala gigante basada en tecnología MPLS), y para ello utiliza la infraestructura física de las grandes telecos, pero de una forma completamente segregada del internet público: por así decirlo, utiliza el mismo canal físico (los mismos “cables gordos” de internet) pero tiene canales lógicos propios, “paralelos” a internet.

Además, algunas zonas pueden tener sus propias “carreteras” internas. Por ejemplo en Europa existe SEPA (Single Euro Payments Area) y SEPA Instant (la versión Fórmula 1 de SEPA). Para transferencias dentro de Europa, no llega a usarse SWIFT. En España específicamente existe Iberpay (SNCE).

Los bancos más pequeños, los que no pueden permitirse usar este tipo de infraestructura, sí usan el internet convencional, pero con cifrado de grado militar.

La banca corresponsal

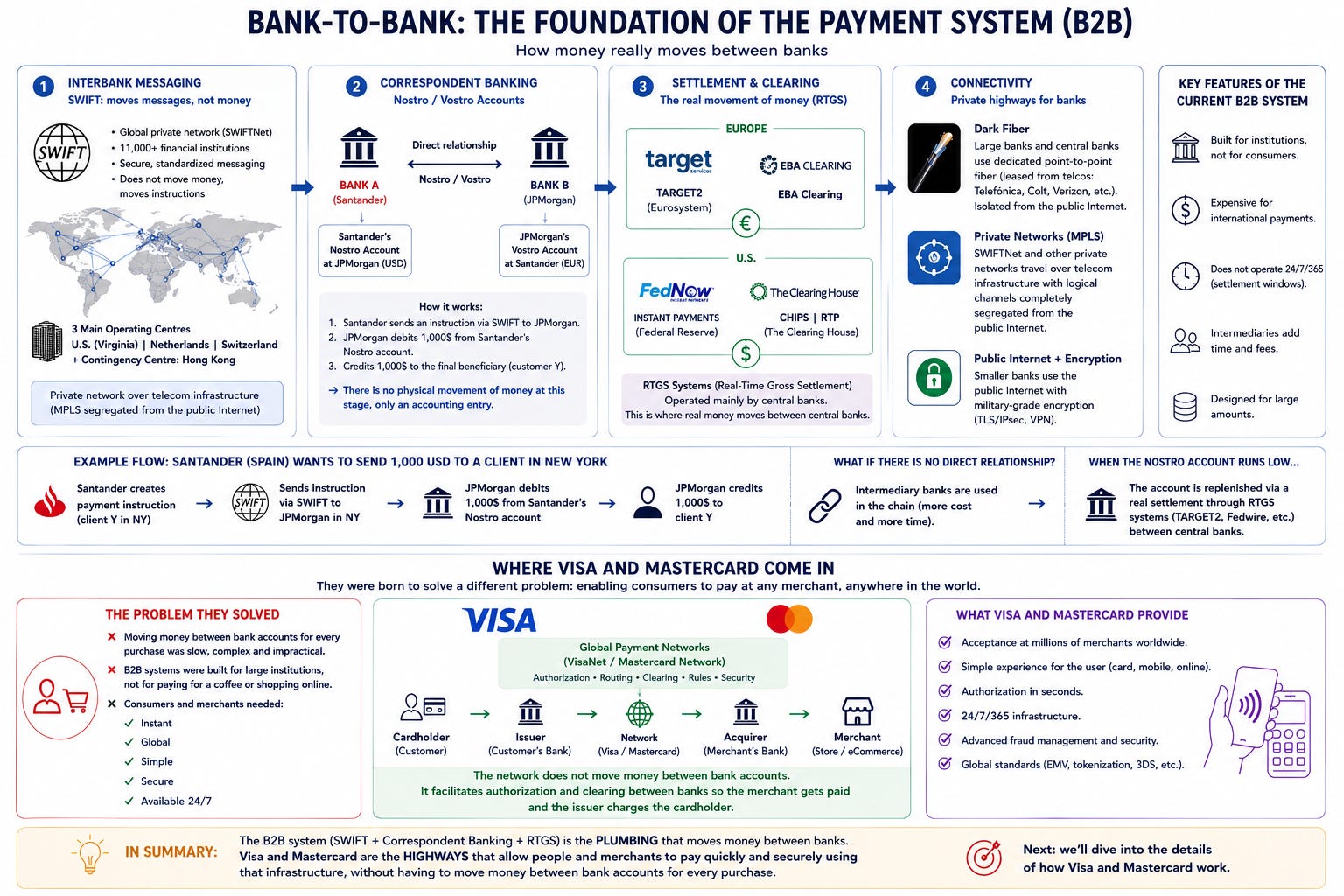

Aquí llega un concepto importante, que es el que realmente explica cómo funciona el sistema: la banca corresponsal. Y algo importante para entender el ecosistema: SWIFT no mueve dinero. Mueve mensajes. Es básicamente un sistema de mensajería ultrasegura entre bancos. El dinero en sí se mueve a través de otro conjunto de actores: las cámaras de compensación.

Mensajería interbancaria.

SWIFT.

Liquidación y compensación (el movimiento real del dinero).

En Europa: TARGET2 (operado por el Eurosistema, el banco central) y EBA Clearing.

En EE.UU: FedNow (el sistema de la Reserva Federal, relativamente reciente) y The Clearing House (opera CHIPS y RTP).

Estos sistemas de liquidación son lo que se conoce como RTGS (Real-Time Gross Settlement), y son operados mayoritariamente por los propios bancos centrales. Son la fontanería real del sistema financiero.

Los grandes bancos internacionales tienen cuentas abiertas unos en otros. El Santander tiene una cuenta con dinero real depositado en JPMorgan (y viceversa). Cuando el Santander quiere mandar dólares a JPMorgan en Nueva York, SWIFT es el canal por el que viaja la instrucción segura: “Oye, JPMorgan, soy Santander. Quítame 1000$ de mi cuenta contigo y dáselos al cliente con cuenta Y”. Cuando el Santander manda esa instrucción por SWIFT, JPMorgan simplemente hace un apunte contable: descuenta el importe de la cuenta que el Santander tiene con ellos y lo abona al destinatario final. No hay movimiento físico de dinero en ese momento, solo un ajuste de saldos.

Y si el banco que quiere enviar no tiene una relación directa con el banco destino, utiliza uno o varios bancos intermediarios que sí la tengan. Eso es lo que hace que algunas transferencias internacionales sean lentas (1-3 días hábiles) y caras: hay que pagar a cada intermediario que toca la cadena.

Ahora bien, si el Santander hace muchas transferencias hacia EE.UU y pocas en sentido contrario, esa cuenta que tiene en JPMorgan se va vaciando. En algún momento hay que reponerla con dinero real, y eso se hace mediante liquidaciones reales entre bancos a través de los sistemas de los bancos centrales: los sistemas RTGS ya comentados, como TARGET2 en Europa o Fedwire en EE.UU. Ahí sí se mueve dinero de banco central a banco central, que es el dinero “real” en el fondo del sistema.

Las limitaciones del sistema Banco-Banco

El sistema que acabamos de describir funciona. Y lleva décadas funcionando. Pero tiene fricciones evidentes: es caro en pagos internacionales, no opera 24/7, y en cuanto sales de tu zona geográfica aparecen intermediarios, tiempos de espera y comisiones que se acumulan. Además, todo este ecosistema está pensado para mover cantidades grandes entre instituciones, no para que tú pagues un café o compres algo por internet.

Y ahí está precisamente el origen de la siguiente capa del ecosistema. Visa y Mastercard no nacieron para competir con SWIFT ni con las cámaras de compensación. Nacieron para resolver un problema completamente distinto: cómo hacer que un particular pueda pagar en cualquier comercio del mundo de forma cómoda, rápida y segura, sin tener que mover dinero entre cuentas bancarias cada vez que compra algo.

Pagos C2B: Del Consumidor al Negocio

En un pago convencional con tarjeta, el flujo lógico es:

Comercio → Gateway → Adquirente → Redes de Pago (Visa/MC) → Banco Emisor

Y el dinero hace exactamente el camino inverso durante la fase de liquidación, por las noches, a través de las cámaras de compensación que ya vimos antes.

Las redes de pago como Visa o Mastercard operan sobre infraestructura privada — básicamente una VPN enorme con contratos millonarios con las operadoras de telecomunicaciones, completamente segregada del internet público. Un retardo de unos pocos milisegundos más allá de lo acordado deriva en indemnizaciones importantes. Lo que ofrecen, en esencia, es velocidad en la autorización del pago y la infraestructura para que después todo cuadre.

La magia del mensaje en 200 milisegundos

Redes como VisaNet o Banknet son capaces de procesar miles de transacciones por segundo con una latencia casi nula. Cuando el cliente pasa la tarjeta por el datáfono, ocurren dos fases que operan a velocidades y en mundos totalmente distintos:

Fase 1: Autorización (tiempo real, menos de 1 segundo)

Un mensaje viaja siguiendo el flujo de software mencionado desde el comercio hasta el banco emisor. El banco dice “este cliente tiene saldo o crédito suficiente, aprobado“. Ese OK bloquea el dinero en la cuenta del cliente y le asegura al adquirente — y por tanto al comercio — que el pago va a producirse. Nadie ha movido un solo céntimo todavía, pero el café ya es tuyo.

Fase 2: Compensación y Liquidación (Clearing & Settlement — diferido, por la noche)

Aquí es donde el “Mundo Tarjeta” se conecta con el “Mundo Transferencia”.

A lo largo del día se van acumulando autorizaciones en cada pago. Al final del día, cuando todos los comercios cierran sus terminales, los adquirentes vuelven a hablar con Visa, Mastercard o la red de pagos correspondiente. Empaquetan millones de transacciones y las mandan para hacer el “neteo”: la compensación entre todos los bancos. Y a través de los sistemas RTGS de los bancos centrales que ya comentamos (TARGET2, FedWire), se realiza el movimiento real del dinero.

Es decir: primero se autorizan y “anticipan” todos los pagos a lo largo del día, y cada cierto tiempo se hace recuento de todo el dinero que realmente tiene que moverse. Las redes de pago hacen la magia de esa compensación.

“A ver, Santander: tus clientes han gastado 10M fuera de tu banco. Pero a los comercios que tienen cuenta contigo les han comprado 2M desde tarjetas de otros bancos. En el neto global del día, estás en negativo por 8 millones. Tienes que pagarlos.”

Y el neteo consiste precisamente en eso: el Santander no hace miles de transferencias para pagar los 10M y recibir los 2M. Simplemente salda su posición neta diaria — los 8 millones — a través del sistema RTGS con el que opera su banco central.

¿Y para qué sirven los adquirentes?

Tras leer las secciones anteriores podría parecer que los adquirentes son solo un intermediario entre el comercio y la red de pagos que chupa del bote. Y efectivamente son un intermediario chupando del bote, pero en las siguientes líneas veremos que realmente se ganan el pan.

Uno podría pensar: si la red de pagos ya hace todo esto, ¿por qué el datáfono no le da los datos del cliente directamente a Visa o a Mastercard para que ellos autoricen y más tarde liquiden el pago? ¿Por qué Apple, Spotify o Uber pagan millones a Adyen en lugar de conectarse directamente a Visa?

La razón principal es que el mundo es caótico. Hay millones de comercios, cada uno con sus particularidades — su zona geográfica, su tipo de negocio, su cliente.

Conectar ese caos con las ultra-estrictas redes de Visa y Mastercard es una pesadilla de ingeniería, regulación, riesgo de fraude y gestión de tesorería. Es como intentar enchufar una tostadora doméstica directamente a una torre de alta tensión. Necesitas un transformador que adapte la potencia, gestione los picos de tensión, te asegure que no salga ardiendo la casa y, además, te agrupe la factura a fin de mes. Ese transformador es el adquirente.

Traductor

El adquirente hace de traductor: toma el formato web de Uber o el código del datáfono de la esquina, lo limpia, lo cifra y se lo entrega a la red de pagos masticado y perfecto. Si la red de pagos tiene un problema en un momento dado, el adquirente retiene la petición y la reintenta, salvando la venta del comercio.

Smart Routing

Si te conectaras directamente a Visa, estarías atrapado en su camino único. Un adquirente global como Adyen hace Smart Routing: cuando metes tu tarjeta en una web internacional, el adquirente analiza en milisegundos de qué banco es la tarjeta, de qué país, qué red es más barata en ese momento. Si ve que procesar el pago por Visa internacional va a costar un 2% y tiene una probabilidad de rechazo del 15% por sospecha de fraude, puede decidir enrutar ese pago a través de una red local o un acuerdo directo con el banco emisor. Esto maximiza la tasa de conversión — que el pago no sea denegado por error —, que es lo que realmente le importa a un comercio online.

Escudo Anti-Fraude

El adquirente asume el riesgo de crédito y fraude del comercio. Por eso, para ser adquirente necesitas una licencia financiera. Adyen analiza la salud financiera de Spotify o de la aerolínea de turno antes de contratarlos. Si la aerolínea quiebra y miles de clientes reclaman sus vuelos, Adyen tiene que devolver ese dinero de su propio bolsillo. Visa no quiere asumir el riesgo de lidiar con millones de comercios; prefiere exigirle responsabilidades a un puñado de adquirentes regulados y que ellos se las arreglen con cada cliente y cada comercio.

Tesorería

Imagina que un comercio vende mil cafés al día a 2€ cada uno. Si Visa liquidara directamente con el comercio, tendría que hacer mil micro-transferencias diarias — ineficiente y carísimo. El adquirente actúa como embudo: recibe de los bancos emisores un único bloque de fondos netos correspondiente a millones de transacciones, descuenta su comisión (más la de Visa y la del banco emisor), y le ingresa al comercio un único pago limpio al día o a la semana. El comercio no concilia nada; solo ve un ingreso diario en su cuenta.

Pagos U2U: Usuario-Usuario (P2P Peer-to-Peer)

El tercer gran bloque del ecosistema es el más cercano al usuario de a pie: mandarte dinero a un amigo para pagar la cena, dividir el alquiler, o saldar una deuda. En teoría es el caso de uso más sencillo de todos — dos personas, dos cuentas, una cantidad. En la práctica, durante décadas fue también el más incómodo, porque exigía conocer el IBAN del otro, esperar un día hábil y rezar para no equivocarse de número.

Lo que ha cambiado en los últimos años es que estos pagos ya no necesitan pasar por las redes de tarjetas. Usan directamente otros raíles bancarios que ya describimos — SEPA Instant, sistemas RTGS, APIs de Open Banking — pero con una capa de software encima que hace que el proceso sea tan rápido y sencillo como mandar un mensaje de WhatsApp.

Los ejemplos más relevantes a nivel global:

Bizum (España): Corre sobre Iberpay y SEPA Instant. En lugar de pedir el IBAN, usas el número de móvil. El dinero llega en segundos.

Zelle (EE.UU.): Consorcio creado por los grandes bancos americanos para competir con las apps de terceros. Opera directamente entre cuentas bancarias, sin saldo intermediario.

Venmo / Cash App (EE.UU.): Modelo diferente — el dinero queda en un saldo dentro de la propia app (lo que se llama “closed-loop” o bucle cerrado) hasta que el usuario decide transferirlo a su banco. Más flexible para el usuario, pero el dinero no está en tu cuenta bancaria real hasta que lo sacas.

Pix (Brasil): Creado directamente por el Banco Central brasileño. Uno de los casos de éxito más llamativos a nivel global — en pocos años se convirtió en el método de pago dominante en Brasil, desbancando tanto a las transferencias tradicionales como al efectivo.

UPI (India): La Unified Payments Interface india es probablemente el ecosistema P2P más grande del mundo por volumen de transacciones. Un caso de libro de cómo la intervención regulatoria puede acelerar la adopción masiva de pagos digitales.

Lo interesante de esta capa, desde el punto de vista inversor, es que es donde más claramente se ve la amenaza para el ecosistema tradicional. Estos sistemas no pagan tasas de intercambio a Visa ni a Mastercard. No necesitan adquirentes. Van directos de cuenta a cuenta. Y en los países donde han despegado de verdad — Brasil, India, China con WeChat Pay y Alipay — la penetración de las redes de tarjetas tradicionales ha quedado estructuralmente limitada.

Conclusión: El mapa antes del territorio

Si has llegado hasta aquí, enhorabuena — y gracias por la paciencia. Era un ladrillazo, lo sé. Pero era un ladrillazo necesario.

El ecosistema de pagos es de esos sectores donde es muy fácil leer titulares (”Visa gana X millones”, “PayPal pierde cuota de mercado”, “las stablecoins van a cargarse a los bancos”) sin tener claro exactamente qué está pasando por debajo. Y sin ese contexto, es muy difícil saber si el titular importa, si el riesgo es real, o si es simplemente ruido.

Lo que hemos visto en este artículo es que el ecosistema tiene tres grandes capas bien diferenciadas. La capa B2B, que es la fontanería real del sistema financiero — SWIFT, corresponsales, cámaras de compensación — y que lleva décadas funcionando pero arrastra fricciones evidentes en los pagos internacionales. La capa C2B, donde Visa y Mastercard construyeron su imperio precisamente para resolver lo que el sistema B2B no podía hacer: que un consumidor pague en cualquier comercio del mundo de forma cómoda y segura. Y la capa P2P, que es la más nueva y la que más claramente amenaza a las capas anteriores, porque va directa de cuenta a cuenta sin necesitar ni redes de tarjetas ni adquirentes.

Y encima de todo esto: disrupción por todos los flancos. Pagos A2A, stablecoins, Open Banking, iniciativas de bancos centrales. Todos atacando alguna de estas capas. Todos con argumentos reales. Ninguno, de momento, con una victoria decisiva.

Y en estos momentos de incertidumbre, estos momentos en que las empresas de un sector están golpeadas, es cuando merece la pena entender y estudiar dicho sector. Porque como decíamos al principio, a río revuelto, ganancia de pescadores.

Eso es precisamente lo que viene en los próximos posts. Tengo en el radar empresas como Visa, Mastercard, Adyen, Fiserv o PayPal — cada una operando en una capa distinta del ecosistema, con modelos de negocio distintos, y con amenazas distintas encima de la mesa. Ahora que tenemos el mapa general, podemos analizar cada empresa con mucho más contexto y más sentido.

Nos vemos en próximos posts. Suscribíos para recibirlos directamente en vuestro email.

Saludos!

English Version

Fishing in the Payments Ecosystem

Everything you need to know about the payments ecosystem before casting your line

They say troubled waters make for good fishing. And if you’ve been scrolling through social media or following economic and investment news lately, you’ve probably noticed that the payments ecosystem is pretty troubled right now:

Fierce competition between traditional players and new entrants.

Constant technological disruption.

Cryptocurrencies and stablecoins pushing in from outside the system.

Central banks making a mess with their own digital initiatives.

Regulation and tax enforcement tightening.

A2A payments (account to account), offered by some acquirers to pay directly from a bank account to another, bypassing much of the traditional ecosystem — leaving out Visa and Mastercard, for example.

Closed-Loop payments, moving balances within the same app.

Artificial intelligence redesigning processes that hadn’t been touched in decades.

And even “tap to pay”, turning your phone into a payment terminal and cutting out hardware that used to be essential.

It’s a world that I’d say is simple at its core, because everything makes sense once you understand it. But right now it’s all a bit tangled. Something that in principle seems straightforward (”I give the order for money to move from source X, usually a bank account, and appear at destination Y, also usually a bank account”) has turned, after decades of development by different players, into a Frankenstein with many layers of functionality piled on top.

When you look at the whole ecosystem together, it feels like it could be massively simplified. And that, in my opinion, is the biggest structural threat to many companies in this sector. With the networks and technologies that existed two decades ago, everything made sense. But with the technology available today — incredibly powerful servers and a fully interconnected world with fast networks — much of the functionality looks redundant: layers that could be eliminated or collapsed, cutting out players that currently get paid just for sitting in the middle.

In upcoming posts I’m going to analyze several companies in this sector, and this article is a necessary introduction to understanding the payments ecosystem in general. In the following sections I’ll try to give a broad overview.

⚠️ Fair warning: this one’s a long read ⚠️

The next sections might be a bit dense, but trust me it’s worth the patience — once you have the context and understand the payments ecosystem, it’s much easier to understand the rationale behind each company: what each one does, how important it is, whether it has a real moat, and why its existence might be under threat.

B2B Movements: Bank-to-Bank

The foundation of this entire ecosystem is the transfer of capital between banks, from one bank account to another. All the other layers — the card networks of Visa or Mastercard, acquirers like Adyen or Fiserv, A2A payments, etc. — could ultimately be seen as add-ons designed to make these bank-to-bank transfers more convenient and secure.

“Transfer between bank accounts” sounds simple enough. In reality, there’s a massive infrastructure underneath that most people know nothing about.

The first thing to understand is that banks don’t communicate over the same internet you use to watch Netflix. The large banks (the so-called Tier 1: JPMorgan, Citigroup, BNP Paribas, Bank of America, Santander...) and central banks use what’s known as dark fiber: optical fiber strands leased long-term from telecommunications operators that are dedicated exclusively to that traffic. Nobody else passes through there. It’s literally a private tube of light from point A to point B. This isolates the network and largely prevents cybersecurity issues.

For international connections between the most important financial institutions, the story is similar but on a larger scale. SWIFT (the cooperative connecting more than 11,000 financial institutions worldwide) hasn’t laid its own cables across the Atlantic. However, it does operate its own private global network (SWIFTNet, a massive VPN based on MPLS technology), using the physical infrastructure of the major telecoms, but in a way that is completely segregated from the public internet: it uses the same physical channels (the same big internet cables) but has its own logical channels running “parallel” to the internet.

Some regions also have their own internal “highways.” In Europe, for example, there is SEPA (Single Euro Payments Area) and SEPA Instant (the Formula 1 version of SEPA). For transfers within Europe, SWIFT isn’t needed. In Spain specifically, there is Iberpay (SNCE).

Smaller banks that can’t afford this type of infrastructure do use the regular internet, but with military-grade encryption.

Correspondent Banking

Here comes an important concept — the one that really explains how the system works: correspondent banking. And something critical to understand about the ecosystem: SWIFT doesn’t move money. It moves messages. It’s essentially an ultra-secure messaging system between banks. The money itself moves through a different set of players: clearing houses.

Interbank messaging.

SWIFT.

Clearing and settlement (the actual movement of money).

In Europe: TARGET2 (operated by the Eurosystem, the central bank) and EBA Clearing.

In the US: FedNow (the Federal Reserve’s relatively recent system) and The Clearing House (which operates CHIPS and RTP).

These settlement systems are known as RTGS (Real-Time Gross Settlement), and are operated mostly by the central banks themselves. They are the true plumbing of the financial system.

Large international banks hold accounts with each other. Santander has an account with real money deposited at JPMorgan (and vice versa). When Santander wants to send dollars to JPMorgan in New York, SWIFT is the channel through which the secure instruction travels: “Hey JPMorgan, this is Santander. Take $1,000 from my account with you and give it to the customer with account Y.” When Santander sends that instruction via SWIFT, JPMorgan simply makes a bookkeeping entry: it deducts the amount from Santander’s account and credits it to the final recipient. No physical money moves at that moment — just a balance adjustment.

And if the sending bank doesn’t have a direct relationship with the destination bank, it uses one or more intermediary banks that do. That’s what makes some international transfers slow (1–3 business days) and expensive: every intermediary in the chain needs to be paid.

Now, if Santander sends a lot of transfers to the US but few in the other direction, the account it holds at JPMorgan gradually empties. At some point it needs to be replenished with real money, and that happens through actual settlements between banks via the central bank systems: the RTGS systems already mentioned, like TARGET2 in Europe or Fedwire in the US. That’s where real central bank money moves — the “real” money at the bottom of the system.

The Limitations of the Bank-to-Bank System

The system we’ve just described works. And it’s been working for decades. But it has obvious friction: it’s expensive for international payments, doesn’t operate 24/7, and as soon as you cross your geographic zone, intermediaries, waiting times and fees start piling up. On top of that, this entire ecosystem is designed to move large amounts between institutions — not for you to pay for a coffee or buy something online.

And that’s precisely the origin of the next layer of the ecosystem. Visa and Mastercard weren’t born to compete with SWIFT or clearing houses. They were born to solve a completely different problem: how to let an individual pay at any merchant in the world, conveniently, quickly, and securely, without having to move money between bank accounts every time they buy something.

C2B Payments: From Consumer to Business

In a conventional card payment, the logical flow is:

Merchant → Gateway → Acquirer → Payment Networks (Visa/MC) → Issuing Bank

And the money flows in exactly the reverse direction during the settlement phase overnight, through the clearing houses we already covered.

Payment networks like Visa or Mastercard operate on private infrastructure — essentially a massive VPN with multi-million dollar contracts with telecom operators, completely segregated from the public internet. A delay of more than a few milliseconds beyond what’s agreed triggers significant penalties. What they offer, in essence, is speed in payment authorization and the infrastructure to make everything balance out afterwards.

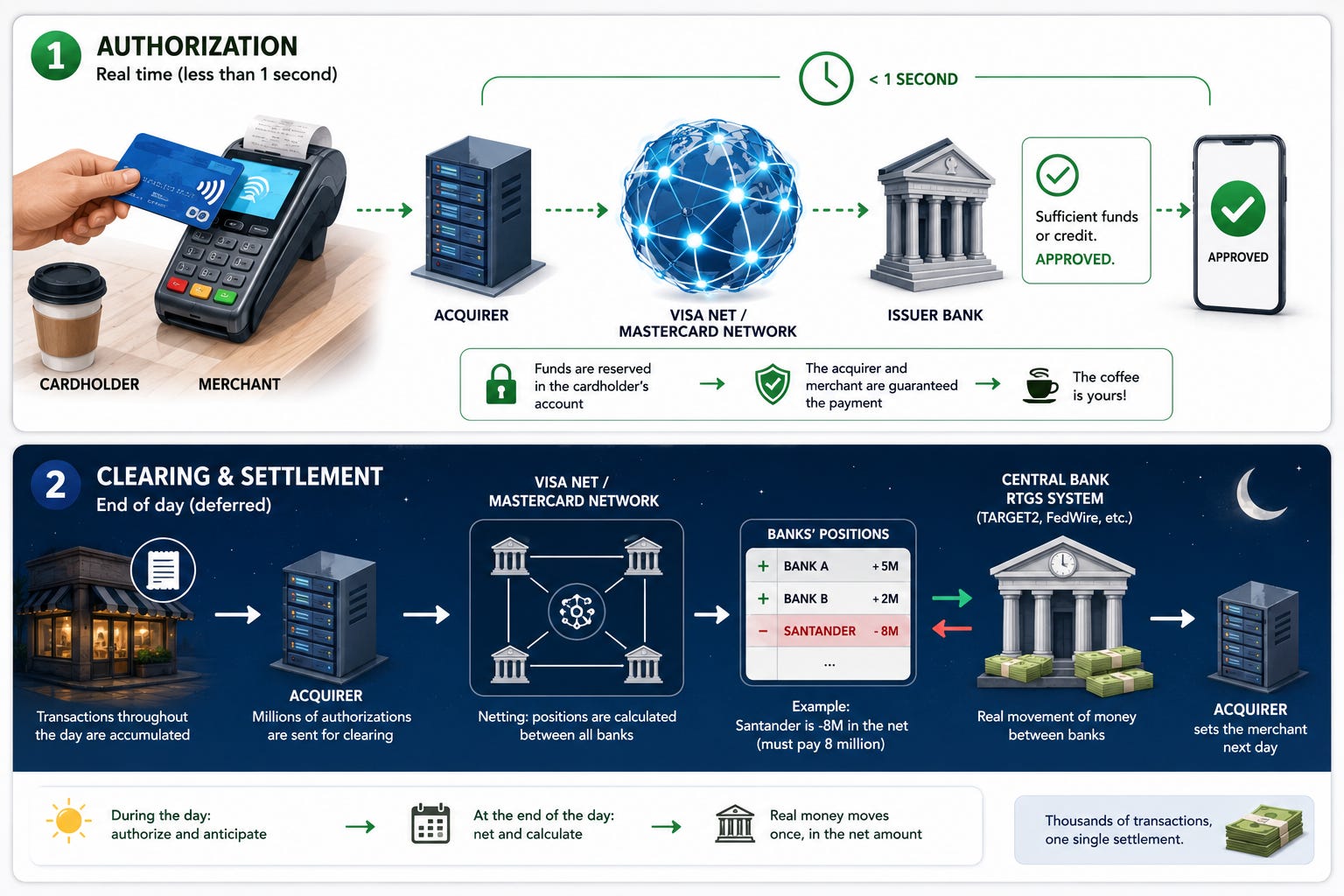

The Magic of the Message in 200 Milliseconds

Networks like VisaNet or Banknet can process thousands of transactions per second with near-zero latency. When a customer swipes their card on a payment terminal, two phases take place operating at completely different speeds and in entirely different worlds:

Phase 1: Authorization (real time, under 1 second)

A message travels following the software flow mentioned above from the merchant to the issuing bank. The bank says “this customer has sufficient balance or credit, approved.” That OK blocks the funds in the customer’s account and assures the acquirer — and therefore the merchant — that the payment will go through. Not a single cent has moved yet, but the coffee is yours.

Phase 2: Clearing & Settlement (deferred, overnight)

This is where the “Card World” connects with the “Transfer World.”

Throughout the day, authorizations accumulate with each payment. At the end of the day, when all merchants close their terminals, acquirers go back to talk to Visa, Mastercard, or the relevant payment network. They package millions of transactions and send them to carry out the “netting”: the clearing between all banks. And through the RTGS systems of the central banks we already covered (TARGET2, FedWire), the actual movement of money takes place.

In other words: all payments are authorized and “pre-confirmed” throughout the day, and periodically a full accounting is done of all the money that actually needs to move. The payment networks perform the magic of that clearing.

“Right, Santander: your customers have spent 10M outside your bank. But merchants who bank with you have received 2M in purchases from other banks’ cards. Your net position for the day is negative 8 million. You need to pay up.”

And netting means exactly that: Santander doesn’t make thousands of transfers to pay the 10M and receive the 2M. It simply settles its net daily position — the 8 million — through the RTGS system it operates with its central bank.

What Are Acquirers Actually For?

After reading the previous sections, it might seem like acquirers are just a middleman sitting between the merchant and the payment network, skimming off the top. And yes, they are middlemen skimming off the top — but in the lines below we’ll see they genuinely earn their place.

You might wonder: if the payment network already does all this, why doesn’t the payment terminal give the customer’s data directly to Visa or Mastercard to authorize and later settle the payment? Why do Apple, Spotify or Uber pay millions to Adyen instead of connecting directly to Visa?

The main reason is that the world is chaotic. There are millions of merchants, each with their own particularities — their geographic region, their type of business, their customer base.

Connecting that chaos to the ultra-strict networks of Visa and Mastercard is a nightmare of engineering, regulation, fraud risk and treasury management. It’s like trying to plug a household toaster directly into a high-voltage power line. You need a transformer that adapts the power, manages the surges, makes sure the house doesn’t catch fire, and on top of that, groups everything into a single monthly bill. That transformer is the acquirer.

Translator

The acquirer acts as a translator: it takes Uber’s web format or the code from the corner shop’s terminal, cleans it up, encrypts it and hands it to the payment network perfectly packaged. If the payment network has a hiccup at any point, the acquirer holds the request and retries it, saving the merchant’s sale.

Smart Routing

If you connected directly to Visa, you’d be locked into their single route. A global acquirer like Adyen does Smart Routing: when you enter your card on an international website, the acquirer analyzes in milliseconds which bank issued the card, which country it’s from, which network is cheapest at that moment. If it sees that processing the payment through international Visa is going to cost 2% and has a 15% rejection probability due to fraud suspicion, it can decide to route that payment through a local network or a direct agreement with the issuing bank. This maximizes the conversion rate — meaning the payment doesn’t get declined by mistake — which is what really matters to an online merchant.

Fraud Shield

The acquirer takes on the credit and fraud risk of the merchant. That’s why you need a financial license to be an acquirer. Adyen assesses the financial health of Spotify or whichever airline before signing them up. If the airline goes bankrupt and thousands of customers claim refunds for their flights, Adyen has to pay that money out of its own pocket. Visa doesn’t want to take on the risk of dealing with millions of merchants; it prefers to hold a handful of regulated acquirers accountable and let them sort things out with each customer and merchant.

Treasury

Imagine a merchant sells a thousand coffees a day at €2 each. If Visa settled directly with the merchant, it would have to make a thousand micro-transfers daily — inefficient and extremely costly. The acquirer acts as a funnel: it receives a single block of net funds from the issuing banks covering millions of transactions, deducts its fee (plus Visa’s and the issuing bank’s), and pays the merchant one clean daily or weekly payment. The merchant reconciles nothing; they just see one daily deposit in their account.

U2U Payments: User-to-User (P2P Peer-to-Peer)

The third major block of the ecosystem is the one closest to the everyday user: sending money to a friend to split a dinner bill, divide rent, or settle a debt. In theory it’s the simplest use case of all — two people, two accounts, one amount. In practice, for decades it was also the most inconvenient, because it required knowing the other person’s IBAN, waiting a business day, and hoping you didn’t mistype a digit.

What has changed in recent years is that these payments no longer need to go through card networks. They use other banking rails we already covered directly — SEPA Instant, RTGS systems, Open Banking APIs — but with a software layer on top that makes the process as fast and simple as sending a WhatsApp message.

The most relevant examples globally:

Bizum (Spain): Runs on Iberpay and SEPA Instant. Instead of sharing your IBAN, you use your phone number. The money arrives in seconds.

Zelle (US): A consortium created by the major American banks to compete with third-party apps. Operates directly between bank accounts, with no intermediary balance.

Venmo / Cash App (US): A different model — the money sits in a balance inside the app itself (what’s called “closed-loop”) until the user decides to transfer it to their bank. More flexible for the user, but the money isn’t in your actual bank account until you move it out.

Pix (Brazil): Created directly by the Brazilian Central Bank. One of the most remarkable success stories globally — in just a few years it became the dominant payment method in Brazil, displacing both traditional transfers and cash.

UPI (India): India’s Unified Payments Interface is probably the largest P2P ecosystem in the world by transaction volume. A textbook case of how regulatory intervention can accelerate mass adoption of digital payments.

What’s interesting about this layer from an investor’s perspective is that it’s where the threat to the traditional ecosystem is most clearly visible. These systems don’t pay interchange fees to Visa or Mastercard. They don’t need acquirers. They go straight from account to account. And in the countries where they’ve truly taken off — Brazil, India, China with WeChat Pay and Alipay — the penetration of traditional card networks has been structurally limited.

Conclusion: The Map Before the Territory

If you’ve made it this far, congratulations — and thank you for the patience. It was a long read, I know. But it was a necessary one.

The payments ecosystem is one of those sectors where it’s very easy to read headlines (”Visa earns X billion,” “PayPal loses market share,” “stablecoins are going to kill the banks”) without really understanding what’s happening underneath. And without that context, it’s very hard to know whether the headline matters, whether the risk is real, or whether it’s just noise.

What we’ve seen in this article is that the ecosystem has three clearly differentiated layers. The B2B layer, which is the real plumbing of the financial system — SWIFT, correspondent banks, clearing houses — and which has worked for decades but carries obvious friction in international payments. The C2B layer, where Visa and Mastercard built their empire precisely to solve what the B2B system couldn’t: letting a consumer pay at any merchant in the world conveniently and securely. And the P2P layer, the newest one and the one most clearly threatening the layers above it, because it goes directly from account to account without needing card networks or acquirers.

And on top of all this: disruption on every front. A2A payments, stablecoins, Open Banking, central bank initiatives. All of them attacking one of these layers. All of them with real arguments. None of them, so far, with a decisive victory.

And in these moments of uncertainty — moments when the companies in a sector are under pressure — is exactly when it’s worth understanding and studying that sector. Because as we said at the beginning, troubled waters make for good fishing.

That’s precisely what’s coming in the next posts. On my radar: Visa, Mastercard, Adyen, Fiserv, and PayPal — each operating in a different layer of the ecosystem, with different business models, and with different threats on the table. Now that we have the general map, we can analyze each company with much more context and clarity.

See you in the next one. Subscribe to receive them directly in your inbox.

Cheers!